The growth of capital expenditures in the memory segment is becoming a key factor in the transformation of the entire semiconductor industry amid the artificial intelligence boom. SK hynix, which is preparing to place depositary receipts on the American market, is using this upcoming IPO as a financing tool for a large-scale investment program estimated at about $67 billion.

The company plans to raise up to $10 billion to strengthen its position in the high-performance memory segment, where the AI infrastructure is the main source of demand. As competitors such as Micron Technology and Samsung Electronics are also increasing investments by tens of billions of dollars, this indicates the beginning of a new investment cycle in which the scale of capital becomes a critical factor for competitiveness.

The technological component of this cycle is increasing the financial burden on market participants. SK hynix’s nearly $8 billion contract with ASML for EUV scanners reflects memory manufacturers’ transition toward more complex technical processes, previously associated mainly with logic chips. The development of the HBM segment and multi-chip layout requires the tight integration of logic and memory, increasing dependence on specialized equipment and related suppliers, including TSMC. As a result, memory manufacturers are forced to not only scale investments but also pursue technological independence, repeating the vertical integration typical of Samsung Electronics.

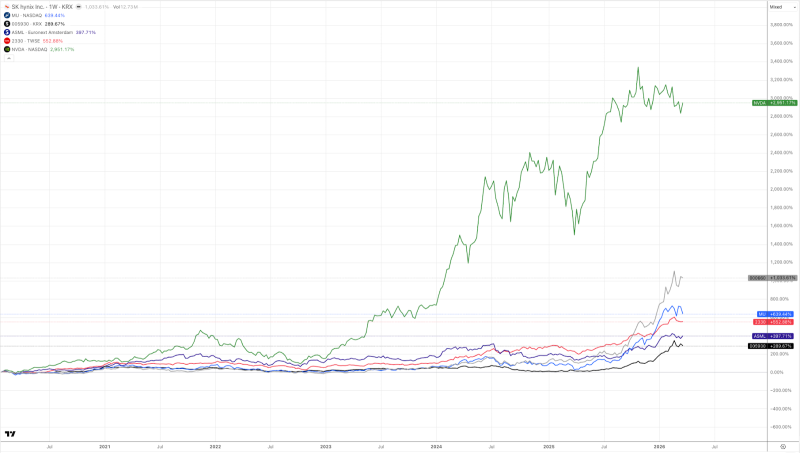

The financial rationale behind these investments is becoming clearer in light of current market dynamics. In 2025, the DRAM segment saw its revenue nearly triple to $150 billion, with growth rates exceeding 50% and establishing memory as a primary beneficiary of the AI boom. At the same time, Micron Technology recorded the strongest growth momentum among the largest players by increasing revenue by more than 50%, strengthening it position on the heatmap, while Nvidia maintained its lead in absolute revenue. Revenue concentration is intensifying as major companies increase their market share faster than others, accelerating industry consolidation and raising barriers to entry for new players.

Rising pressure is highlighting the need to better align investment cycles with actual demand. As revenue growth in the memory segment is currently driven more by a surge in prices rather than production volumes, the market remains sensitive to a potential correction. In an environment where the key players are simultaneously scaling capital expenditures, there is a risk of oversupply in the medium term, especially if the growth rate of the AI infrastructure slows down. This heightens the dependence of companies on external financing, including public capital markets, which explains SK hynix’s recent move to pursue a U.S. listing.

Together, these dynamics are reshaping the investment profile of the semiconductor sector. AI demand for memory continues to support revenue growth and drive large-scale investments in manufacturing and technology. Meanwhile, increased capital expenditures, technological dependence on a limited number of suppliers, and high market concentration increase the risks of cycling and possible overheating. For investors, this means moving from a phase of rapid growth to a more balanced valuation, where the ability of companies to align investments with real demand and maintain efficiency amid intensifying competition and rising technological costs becomes increasingly important.