In the rapidly changing financial world of 2026, a B2B crypto on-ramp and off-ramp solution is a key link that connects conventional fiat systems to the digital asset economy. For businesses, this is not just about currency conversion availability; it also calls for a powerful system that can support the supply of liquidity, technical integration, and strict compliance with regulatory norms.

The primary objective of this article is to assess Paybis from a functional and infrastructure standpoint, concentrating on its potential as the best crypto off-ramp provider for B2B clients instead of its retail interface.

Paybis On-Ramp and Off-Ramp Infrastructure Overview

Paybis is a high-volume infrastructure provider that supports a large ecosystem of fiat and digital assets industries through corporate integration. The company’s B2B platform has an architecture capable of handling institutional-level volumes, with a reported annual processing volume of more than $1.2 billion in 2025.

The table below lists the main elements of Paybis B2B infrastructure:

| Component | Business Function |

| On-Ramp | Fiat to crypto conversion |

| Off-Ramp | Crypto to fiat settlement |

| Payment Methods | 20+ methods including cards, bank transfers (SEPA, ACH, Swift), and APMs (Revolut Pay, PayPal, etc.) |

| Asset Support | 90+ cryptocurrencies, including BTC70+ fiat currencies |

| Integration Type | Direct URL, API checkout, Web/iOS/Android SDK, and White-label OTC |

| Regulatory Registrations | FinCEN (USA), FINTRAC (Canada), Revenue Chamber in Katowice (VASP Poland) |

| Compliance | AML/KYC framework, FATF, and GDPR |

| Geographic Coverage | 180+ countries and 48 US states |

This infrastructure enables companies to avoid the intricacies of making their own exchange rails from scratch. Paybis, boasting a platform uptime of around 99.4%, offers a dependable setting for businesses seeking continual access to bitcoin and other main market assets. The system is speed-oriented, with settlement regularly taking less than a minute, allowing users to leverage Bitcoin dominance when it matters the most.

Business Integration and Transaction Processing

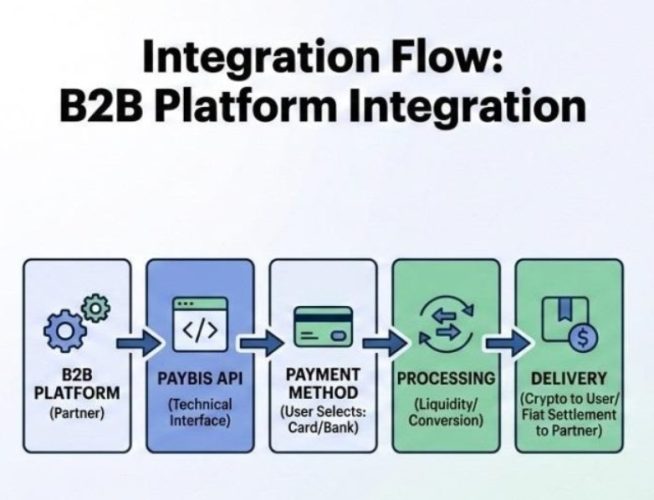

With B2B clients, the integration journey is turned into a quick deployment, with many projects going live within 48 hours. Companies can pick simple integrations, such as a direct URL or more sophisticated, deeply embedded ones via API or SDKs. This diversity not only permits different levels of UX customization but also offers the partners the possibility to white-label the service so that it is presented as their own brand.

Integration Flow Diagram:

The technical implementation centers around the KYC reliance concept, where the onboarding and compliance of the partner’s clients can be done by Paybis, or the partner can simply share their existing KYC data. This modular approach helps to minimize the technical debt of businesses; at the same time, the transaction processing remains compliant with global standards.

Settlement Flow and Payment Infrastructure

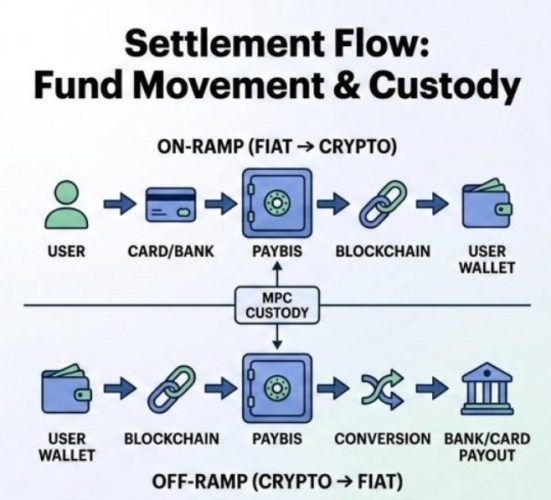

The transfer of money within the Paybis ecosystem is done using a Multi-Party Computation (MPC) custody model, which guarantees that the assets remain safe throughout the conversion process. The settlement flow is split into on-ramp and off-ramp paths to cater to the differing needs of each one.

Settlement Flow:

Timing factors significantly depend on the payment method chosen; for example, card transactions occur almost instantly, but some bank transfers have to rely on the traditional clearing windows. Paybis deals with these dependencies in several ways: it has an overall transaction success rate of about 90% and an authorization rate exceeding 75%.

Regulatory Framework and Risk Controls

Compliance forms the foundation of Paybis B2B model. They keep their registrations in several major jurisdictions, including MSB status in the US and Canada. Their risk management strategy comprises multiple layers of measurable controls that are focused on preventing fraud and protecting data integrity.

| Layer | Control Mechanism |

| KYC | Identity verification in under 2 minutes |

| AML | Continuous transaction monitoring and screening |

| Payment Security | PCI DSS Level 1 compliance |

| Jurisdiction | Region-based compliance (FinCEN, FINTRAC, VASP) |

| Risk Monitoring | AI-powered fraud prevention, including velocity checks and IP controls |

Since these controls are embedded within the API, it follows that any business implementing the solution will, by default, adhere to these security standards. In essence, this Compliance as a Service approach is an excellent boon to those businesses that are resource-strapped to the extent of being incapable of managing separate regulatory registrations in more than 180 countries.

FAQs

Is Paybis a crypto exchange?

Paybis is indeed a cryptocurrency exchange. Besides offering retail services, it also caters to B2B clients by providing specialized infrastructures for on-ramping and off-ramping

Is Paybis regulated?

Paybis is regulated and registered with several authorities, including FinCEN in the US, FINTRAC in Canada, and the Revenue Chamber in Katowice, Poland.

What are the pros and cons of Paybis?

- Pros: Wide geographical coverage (180+ countries), fast integration (<48h), support for multiple payment methods (20+), and PCI DSS Level 1 security.

- Cons: Though they offer services in many countries, some of their licenses, like MiCA in Latvia and a PSP application in Canada, are still pending.

Who is the owner of Paybis?

Paybis was founded by Innokenty Isers and Konstantins Vasilenko.

Learn More About Paybis Business Solutions

Thinking about Paybis as your B2B partner in 2026? Then you should focus on these three aspects mostly: how extensive its infrastructure is (over 90 crypto assets and more than 70 fiat currencies), how thorough its compliance measures are (MSB registrations in the major markets), and how easily it can be integrated (< 48 hours to go live).

The platform’s readiness to support corporate transaction limits, which in some cases can reach $5 million, makes it a viable option for businesses intending to scale up. In the end, the choice to integrate should hinge on a technical check of their API docs and an assessment of how well their compliance model across multiple jurisdictions fits your particular business area.