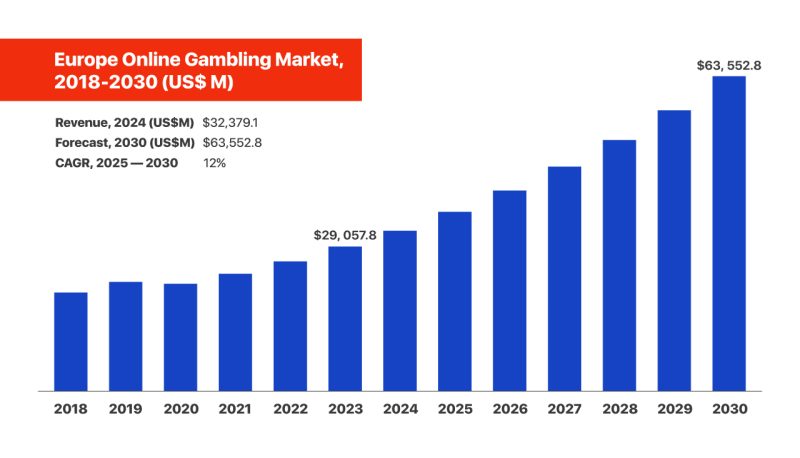

The online casino Europe market is expanding quickly, depending on the methodology used by different research firms, projections vary, but the direction is consistent: up. The European online gambling market generated USD 32,379.1 million in 2024 and is forecast to reach USD 63,552.8 million by 2030. The same outlook projects the market will grow at a 12% CAGR from 2025 to 2030.

Sports betting was the largest revenue-generating type in 2024 and is also the fastest-growing type for the forecast window. Country-wise, it highlights that the UK is expected to register the highest online casino Europe CAGR from 2025 to 2030.

Overview of the EU Online Gambling Market

The EU market is not “one law, one license.” It’s a patchwork of national frameworks, but it still behaves like a single digital ecosystem because operators, payment providers, and player habits are increasingly cross-border. EGBA’s EU market materials on online casino Europe emphasize how regulation, channelization (moving consumers into licensed products), and consumer protection standards are central to market development.

At the same time, Europe’s gambling economy is large even before you isolate the online slice. EGBA states that in 2024, the online casino Europe industry achieved a gross gaming revenue of 123.4 billion euros, representing a 5% increase from 2023. This is important because the online industry is increasing in a large market, and in many countries, the online industry is gaining market share from the brick-and-mortar industry.

Key Contributing Countries

Different countries matter for different reasons: some are big in absolute revenue, others lead in online casino Europe penetration, and others are “swing markets” where regulation is still changing the pace of digital growth.

| Country | Short definition | Core numbers | Note |

| Italy | Scale leader | EGBA’s country comparison states that Italy was Europe’s largest gambling market in 2023 with a total GGR of €21.0 billion.But Italy’s online share, per the same EGBA summary, is comparatively modest: Italy’s online revenue is €4.6 billion and its online share is 21.7%. | In practical terms, Italy is huge, but still not “mostly online,” which leaves room for continued digital migration. |

| United Kingdom | Online powerhouse | EGBA notes the UK’s total GGR was €19.8 billion in 2023 and highlights particularly strong online penetration: €11.1 billion in online revenue | This scale and maturity help explain why many observers consider the UK the reference market for the best online casino Europe product development, strong compliance, strong competition, and constant UX experimentation. |

| Germany | Land-based heavy, online rising | Germany’s total GGR at €14.4 billion in 2023 with an online share of 22.6%. | Germany’s importance is strategic: a relatively low online share in a very large market means that even small shifts toward online casino Europe can move European totals. |

| France | Large and stable, shaped by product rules | EGBA puts France’s total GGR at €14.0 billion in 2023 and its online revenue at €3.8 billion. | France is often described as “stable” because regulation strongly shapes what can scale online, but the overall digital trajectory is still upward as consumers adopt online betting formats. |

| Hungary | Smaller market, clear growth story | The market research summary estimates Hungary’s total market size at about €1.56 billion in 2025 and the online segment at roughly €563 million in 2024, with forecasts through 2029 and an online CAGR around 5.5%. | Hungary is a useful case because it shows how mid-sized markets develop once demand, regulation, and digital product quality align. |

| Nordics | Penetration leaders | The online share ranges as high as 68.3% in Sweden, with Finland and Denmark both at 68.1%. | These are the “proof markets” for what high online penetration looks like when digital payments, broadband/mobile usage, and regulated access come together. They often influence how best online casino Europe operators design onboarding, safer gambling prompts, and mobile-first UX. |

In competitive acquisition, promos matter, including offers framed around no deposit bonus Hungary, but the long-term winners tend to be those that combine a trusted licensed setup with frictionless payments and responsible gambling tooling. Online gambling in Europe is not driven by one country alone. Europe’s growth is the sum of (1) mature markets like the UK scaling product innovation, (2) massive hybrid markets like Germany and Italy shifting share from land-based, and (3) high-penetration markets like the Nordics setting the operational benchmark.

Europe Online Gambling Market Analysis

Several forces keep pushing the online casino Europe market forward, and you can see them in both market totals and online/land-based splits:

- Online is increasingly responsible for the growth in overall European gambling revenue. EGBA reports that provisional online GGR rose 11.7% year-on-year to €47.9 billion in 2024, representing about 39% of total GGR. That same breakdown states gaming accounted for €24.6 billion, with €23.2 billion attributed to online casino Europe-type games (including slots), and that online casino Europe games drew 45% of online GGR in 2024. Those details matter because they show the engine of monetization. Casino-style online products sit at the center of European gambling sites’ online revenue.

- Regulation is a growth driver and a cost factor at the same time. The European regulatory environment is still fragmented, which means there are different licensing requirements, product requirements, taxation schemes, and advertising schemes per country. That raises compliance costs and slows cross-border scaling. At the same time, clear licensing tends to increase consumer trust and channel users away from unregulated sites into regulated online casino Europe environments.

- Mobile adoption and product innovation keep widening the addressable audience. Market research groups disagree on exact CAGR numbers, but even conservative projections describe steady expansion.

In practice, growth is being distributed across better UX, faster payments, and more personalized offers, the features users associate with the best online casino in Europe.

Europe Online Gambling Market Trends

The most visible trend is that “online” is no longer one channel. It’s the default. Platforms are built around mobile onboarding, quick KYC, and product funnels that move players between sportsbook and online casino Europe offerings without friction. Operators are also refining localization:

- Language;

- Payments;

- Customer support hours;

- Game libraries tailored to each country’s preferences.

It’s a competitive necessity if a brand wants to be perceived as the best online casino in Europe rather than just a general online casino. Of course, at the same time, there are increasing standards being set in terms of responsible gambling, AML detection, and marketing. This, in turn, drives the need for better detection tools and transparency in the way that an online casino Europe operates, which again appears to favor larger, more compliant operators or the best online casinos in Europe.

AI and Data Analytics Transforming the Online Gambling Landscape

AI and analytics are moving from “nice-to-have” into core infrastructure. At the market level, the reason is simple: online growth is strong, and operators need to fight churn while meeting stricter compliance requirements. EGBA’s market context emphasizes consumer protection and regulated markets, while the revenue shift toward online (and the size of the online slice) underscores why optimization matters. In practical terms, AI is used to:

- Personalize content;

- Recommend games;

- Tailor promotions;

- Detect unusual betting behavior;

- Flag risky play patterns earlier.

They all support retention and safer gambling obligations. For a competitive online casino Europe operator, data is now part of the product.

Favorable Government Policies

Where regulation is clear, the market tends to channel users into licensed services faster. EGBA’s reporting on market structure and national shares shows how widely online adoption differs by country, from 68.3% online share in Sweden to 14.2% in Spain. That gap is a policy story as much as a consumer story: licensing design, product permissions, enforcement intensity, and advertising rules all change the speed of digital transition.

The macro picture is that Europe’s total market is large (€123.4bn GGR in 2024) and still growing (+5% YoY). Governments that create predictable licensing and enforcement frameworks tend to:

- Attract investment;

- Improve consumer protection standards;

- Reduce the appeal of offshore sites.

All of these strengthen legitimate online casino Europe over time.

Cryptocurrency Integration in Online Gambling Payments

Crypto payments are gaining attention in the wider gambling industry because they can offer fast settlement and different privacy expectations compared to traditional rails. However, adoption across Europe is uneven because national rules around crypto transactions, AML, and payment processing vary. The clearest evidence point here is not “every online casino Europe accepts crypto,” but that the broader digital gambling economy is now large enough that payment innovation is a strategic battleground. In markets where regulators permit it, and operators can meet AML requirements, crypto can become another payment option, but not a universal standard across European online gambling yet.

Expanding Esports Betting and Its Role in Gambling’s New Frontier

Esports betting is often described as one of the most dynamic growth pockets in online wagering, mainly because it maps naturally to younger, digital-first users, the same audiences driving mobile gambling adoption. While EGBA’s country-level snapshot focuses on national revenue and online share, it also indirectly explains why esports matters: in high-penetration online markets, product variety becomes a retention tool, and esports is a natural extension of that.

From an operator perspective, esports is also a way to diversify beyond traditional sports calendars and to create year-round engagement, important in a market where online growth is strong, and competition amongthe best online casino Europe is intense.